Increasing the security of your benefits

You may remember that the DCL Section took out an insurance contract with Rothesay Life Plc (“Rothesay”) in late 2021. We are now pleased to confirm that in December, the Trustee signed a second insurance contract with Pension Insurance Corporation Plc (PIC) for the Dow Section – read more below.

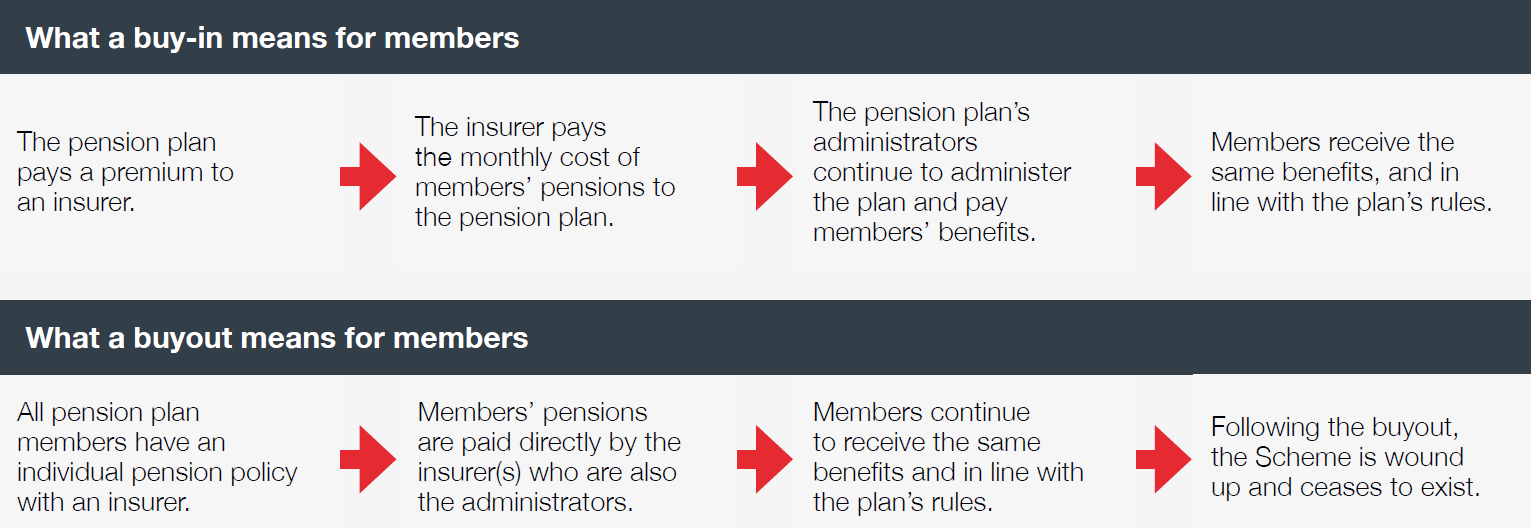

Under these contracts, known as buy-ins, Rothesay and PIC respectively make payments to the Plan to meet the monthly cost of paying members’ pensions. Members do not see a difference. So, what does it really mean for the Plan?

Reducing risk

The buy-ins have transferred the risks in relation to the Plan if investment markets underperform, inflation is higher than expected or members live longer than expected to Rothesay and PIC. Both insurers are well positioned to manage this future uncertainty and as two of the UK’s largest pensions’ insurance specialists are expert in managing these risks and benefit from other economies of scale. They are also bound by strict regulatory requirements.

Through the buy-ins, the Trustee has transferred risks to Rothesay and PIC, but nothing changes for members:

The Trustee continues to have overall oversight of the Plan.

Why have the two Sections agreed buy-ins with two different insurers?

Due to the different funding positions of the Sections, the Trustee has entered into the buy-in policies for each Section at different times. For each transaction, the Trustee carried out detailed due diligence before entering into the buy-in. Rothesay and PIC were chosen, following a competitive pricing and selection process, based on what was best suited for the Section and the relevant membership at the time.

Looking ahead for the DCL Section

Under a buy-in, the pension scheme continues to incur running costs. The only way to fully lock down costs is to move to a ‘buyout’ where full responsibility for paying benefits directly to members is transferred to the insurer. This means that each member holds an individual pension policy with the insurer and receive payments directly from them. As with a buy-in, members’ benefits do not change due to a buyout.

Since the DCL buy-in policy was secured three years ago, work has been ongoing to verify member data following the buy-in, to help ensure members’ entitlements are fully covered by the Rothesay policy.

Together with the Company, the Trustee is considering if, and then when, a buyout may be right for the DCL Section. This is a complex process with a lot of actions required before buyout can take place. We will continue to update DCL members on any developments. In the meantime, the Plan will continue to receive income from Rothesay each month that matches the amounts we are paying to DCL Section members.

More about the buy in for the Dow Section

As mentioned in past editions of Spotlight, the Trustee is committed to reducing risk across the Plan and has been reviewing the market for suitable investments to do so for the Dow Section. As mentioned in the introduction, we are pleased to confirm the Trustee has entered into an insurance contract with PIC following a detailed process to undertake due diligence and select an insurer and negotiate appropriate cover. Going forward we will work with PIC to undertake an exercise to check, and verify, member data to ensure the insurance policy accurately reflects members’ entitlements (as per the process described above for the DCL Section). This is an important step and is likely to take some time.

To reiterate that your benefits are not affected by this insurance contract. Read more about the reasons for a buy in above.

Protecting your data

To complete the buy-in with PIC, we needed to provide them with information about the Dow Section members and their benefits. We take the protection of your personal data very seriously and sharing this information was in line with the Plan’s Data Protection Privacy Notice (see www.mydowpension.co.uk/dow-services section/document-library for a copy). Under the terms of the General Data Protection Regulations (“GDPR”), PIC is now a Data Controller and you can find a copy of its Privacy Notice at www.pensioncorporation.com/content/dam/pic/corporate/documents/privacynotices/PIC-privacy-notice-pic-buy-in.pdf

Keeping your details up to date

You should always keep us up to date on any changes to your personal circumstances and contact details so we can keep in touch when we need to. We encourage all members to review their current information online. If you have any further questions about this article, please get in touch.

Guaranteed Minimum Pension reconciliation (GMPr) and GMP equalisation (GMPe)

The Trustee continues to work with their advisors to complete the work on the ongoing GMPr and GMPe projects.

For DCL section members you may have now been contacted if you were impacted.

Letters went out to most members affected by GMPe in April. A small group of members are still to have their pensions reviewed as part of the GMPe project (mainly those retiring in the last year) and we expect this final phase of the project to be completed before the year end. For Dow Services Section members these projects are still ongoing and the Trustee will be in touch in the future regarding this.

Dow Services Section – Fidelity fund changes

The Trustee recently agreed to make some changes to the Fidelity Global Growth Fund and the Fidelity Global Growth Fund (UK Focus) with the aim of improving risk-adjusted returns for members.

The changes to the Global Growth Fund will not impact the Fund’s aim which is to provide long term capital appreciation through investment primarily in the shares of companies around the world. The total expense ratio on the Global Growth Fund will increase from 0.73% to 0.96% as a result of the changes; however, the Trustee took the level of charges into account when considering whether these changes were in members’ interest.

The changes to the Global Growth Fund (UK Focus) will mean the Fund’s aim will change slightly. From providing long term capital appreciation through investment primarily in the shares of companies around the world but with a bias towards UK equities, this will change to providing long term capital appreciation through investment predominantly in the shares of UK companies. The total expense ratio on the Global Growth Fund (UK Focus) will reduce from 0.55% to 0.53% as a result of these changes.

The changes to these funds happened automatically during November. You do not need to take any action, unless you feel these funds are no longer suited to your investment needs. If you wish to make any amendments to your investment strategy, please contact Capita on 0333 038 4069 or online at portal.hartlinkonline.co.uk/mydowpension

Consolidation of the Dow Services Section Additional Voluntary Contribution (AVC) arrangements

If you held AVCs with Aviva, Coventry Building Society, Legal & General Investment Management Limited, Prudential, Santander, or Utmost Life and Pensions (the Dow Services Section legacy providers), we wrote to you earlier in the year to confirm that your AVCs would be moved to the Plan’s DC Section, unless you opted out. The project to move funds is now nearing completion and unless you opted out, your AVCs have already been invested in, or are about to be invested in, the Alliance Bernstein Target Date Fund that matches your selected retirement date. The Trustee made these changes in order to improve value for members. If your AVCs have been moved to the DC Section, you may wish to review how they are now invested to ensure this suits your investment needs. If you wish to make any amendments to your investment strategy, or change your selected retirement age, please contact Capita on 0333 038 4069 or online at portal.hartlinkonline.co.uk/mydowpension

Going digital

This year’s newsletter has come to you by post, but we would like to send future editions via email. There are a number of reasons for this. Firstly, we would like to be able to contact you quickly with important pension information as well as any urgent situations that may arise that we need to notify you of. That is much easier to do if we hold email addresses for our members.

Secondly, the carbon footprint of sending out information digitally is far smaller than our current method of print and postage. The Trustee has a responsibility to ensure we’re using the Plan’s resources prudently, as well as considering environmental factors.

Thirdly, if you change address and forget to tell us, important information about your benefits could be missed. By contrast, if you change your email address without telling us, then we are likely to get a no-delivery message.

For members of the Dow Services Section, the easiest way to sign up for digital communications and ensure you do not miss out on any important updates is by registering for your online member portal at portal.hartlinkonline.co.uk/mydowpension

For members of the DCL Section, you can opt in to digital communications by emailing your details to DCLPensions@aon.com